LARS Library: Least Angle Regression laSso Library

Frank Vanden Berghen

The PDF version of this page is available here.

You can download here the

LARS library ( v1.06 - released 2/10/2007) (new binaries that works on any windows-matlab

version).

Let's assume that we want to perform a simple identification task. Let's assume

that you have a set of  measures

measures

. We want to find a function (or

a model) that predicts the measure

. We want to find a function (or

a model) that predicts the measure  in function of the measures

in function of the measures

. The vector

. The vector

has several names:

has several names:

is the regressor vector.

is the regressor vector. - is the input.

- is the vector of independent variables.

has several names:

- is the target.

- is the output.

- ( is the dependant variable).

The pair  has several names:

has several names:

- is an input

output pair.

output pair.

- is a sample.

We want to find  such that

such that  . Let's also assume that you know that

. Let's also assume that you know that  belongs to the family of linear models. I.e.

belongs to the family of linear models. I.e.

where

where

is the dot product of two vectors and

is the dot product of two vectors and  is the constant term. You can also write

is the constant term. You can also write

where

where

and are describing . We will now assume, without loss of generality, that

and are describing . We will now assume, without loss of generality, that  . We will see later how to compte if this is not the case.

. We will see later how to compte if this is not the case.  is the model that we want to find. Let's now assume

that we have many input

output pairs. i.e. we have

is the model that we want to find. Let's now assume

that we have many input

output pairs. i.e. we have

We want to compute such that

. Using matrix notation, is the solution of:

. Using matrix notation, is the solution of:

|

(2) |

where

is a matrix containing on each line a different

regressor and

is a matrix containing on each line a different

regressor and

contains all the targets. The columns of

contains all the targets. The columns of  contain the independent variables or, in short, the variables.

If

contain the independent variables or, in short, the variables.

If  , we can compute using a simple Gauss-Jordan elimination. That's not very interesting.

We are usually more interested in the case where

, we can compute using a simple Gauss-Jordan elimination. That's not very interesting.

We are usually more interested in the case where  : when the linear system

: when the linear system  is over-determined. We want to find

is over-determined. We want to find  such that the Total Prediction Error (TPError) is

minimum:

such that the Total Prediction Error (TPError) is

minimum:

TPError |

(3) |

If we define the total prediction error

TPError as

Sum of Squared Errors

where

is the

is the  -norm of a vector, we obtain the Classical Linear Regression

or Least Min-Square(LS):

-norm of a vector, we obtain the Classical Linear Regression

or Least Min-Square(LS):

Classical Linear Regression: is the solution to:

Such a definition of the total prediction error

TPError can give un-deserved weight to a small number of bad samples.

It means that one sample with a large prediction error is enough to change

completely (this is due to the squaring effect that ``amplifies'' the

contribution of the ``outliers''). This is why some researcher use a  instead of a

instead of a  :

:

Robust Regression: is the solution to:

where  is the absolute value. We will not discuss here

Robust regression algorithms. To find the solution of a classical Linear

Regression, we have to solve:

is the absolute value. We will not discuss here

Robust regression algorithms. To find the solution of a classical Linear

Regression, we have to solve:

Since

is a scalar, we can take its transpose without changing

its value:

is a scalar, we can take its transpose without changing

its value:

. We obtain:

. We obtain:

The equation 4 is the well-known normal equation.

On the left-hand-side of this equation we find

: the correlation matrix.

: the correlation matrix.  is symmetric and semi-positive definite (all the eigenvalues of are

is symmetric and semi-positive definite (all the eigenvalues of are  ). The element

). The element

is the correlation between column

is the correlation between column  and column

and column  (where

(where  stands for column of ). The right-hand-side of equation 4 is also

interesting: it contains the univariate relation of all the columns of (the variables) with the target .

stands for column of ). The right-hand-side of equation 4 is also

interesting: it contains the univariate relation of all the columns of (the variables) with the target .

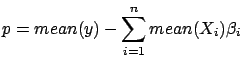

We did previously the assumption that the constant term of the model is zero. is null when  and

and

where

where

is the mean operator and is the

is the mean operator and is the  column of . Thus, in the general case, when

column of . Thus, in the general case, when  , the procedure to build a model is:

, the procedure to build a model is:

- Compute

where

where

is the ``standard deviation'' operator.

is the ``standard deviation'' operator.

- Normalize the target:

- Normalize the columns of :

- Since the columns of

have zero mean, and since

have zero mean, and since  has zero mean, we have . We can thus use the normal equations:

has zero mean, we have . We can thus use the normal equations:

to find

to find

. All the columns inside have a standard deviation of one. This increase numerical

stability.

. All the columns inside have a standard deviation of one. This increase numerical

stability.

- Currently,

has been computed on the ``normalized columns''

and . Let's convert back the model so that it can be applied on the

un-normalized and :

and . Let's convert back the model so that it can be applied on the

un-normalized and :

From now on, in the rest of this paper, we will always assume that (data has been normalized).

One simple way to solve the normal equations 4

is the following:

- Compute a Cholesky factorization

of

of  . i.e. Compute such that is a lower triangular matrix and such that

. i.e. Compute such that is a lower triangular matrix and such that  .

.

- Let's define

. Then we have:

. Then we have:

(the last equality comes from equation 4).

This last equation (

(the last equality comes from equation 4).

This last equation (

)can be solved easily because

)can be solved easily because  is triangular. Once we have found

is triangular. Once we have found  , we solve

, we solve

to find (this is also easy because is triangular).

to find (this is also easy because is triangular).

Unfortunately, the above algorithm is not always working properly. Let's consider

the case where  . i.e. the variables and are 100% linearly correlated together. In this case, we will have

. i.e. the variables and are 100% linearly correlated together. In this case, we will have

.

.  can be any value at the condition that

can be any value at the condition that

(so that we obtain

(so that we obtain

and none of the columns and are meaningful to predict ). Thus, can become extremely large and give undeserved weight to the

column . We have one degree of liberty on the 's. This difficulty arises when:

and none of the columns and are meaningful to predict ). Thus, can become extremely large and give undeserved weight to the

column . We have one degree of liberty on the 's. This difficulty arises when:

- A column of is a linear combination of other columns.

- The rank of A is lower than

.

.

- The matrix is not of full rank .

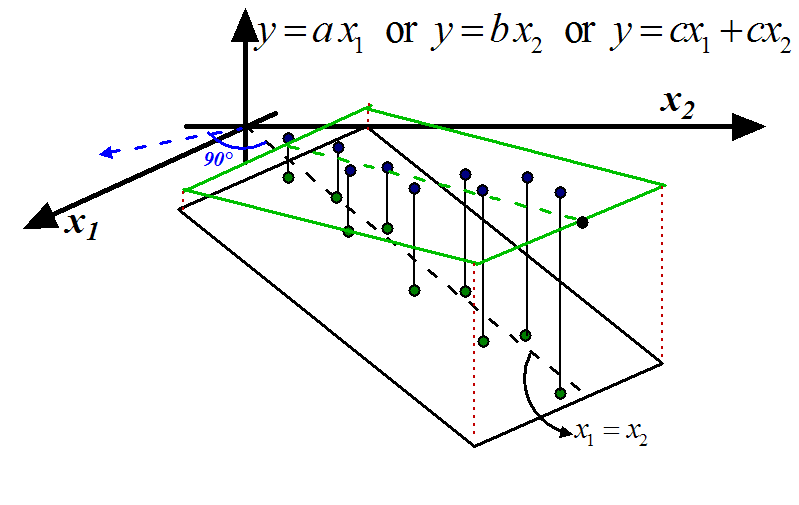

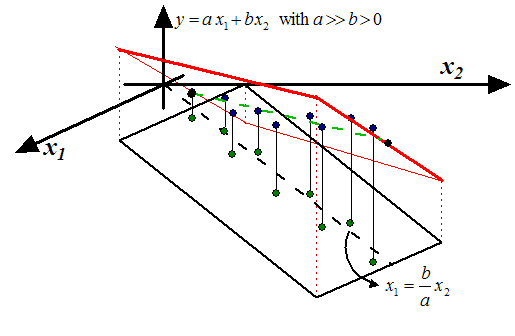

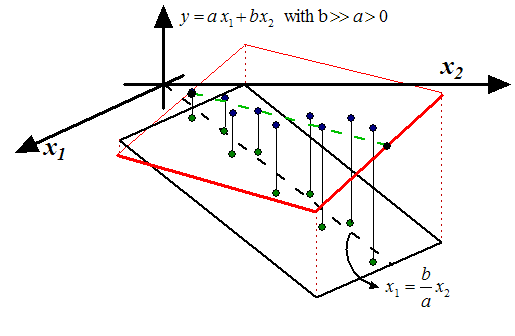

This problem is named the ``multi-colinearity problem''. It is illustrated in

figure 1 and 2.

Figure 1: Stable Model

|

Figure 2: Unstable Models

|

The blue points inside figures 1 and 2

are the samples. The green points are the lines of

(the inputs) and the heights of the

blue points are the targets (

(the inputs) and the heights of the

blue points are the targets (

)(the output). There is a linear correlation between

)(the output). There is a linear correlation between

and

and  :

:

. In the ``blue direction'' (perpendicular to

the black dashed line), we do not have enough reliable information to decide if

the output should increase or decrease. Inside figures 1

and 2, a model is represented by a plane. In this situation, the ideal model

that we want to obtain, is drawn in green in figure 1

(the plane/model is ''flat'': there is no un-due variation of in the ``blue direction''). The equation of the ideal model is either:

. In the ``blue direction'' (perpendicular to

the black dashed line), we do not have enough reliable information to decide if

the output should increase or decrease. Inside figures 1

and 2, a model is represented by a plane. In this situation, the ideal model

that we want to obtain, is drawn in green in figure 1

(the plane/model is ''flat'': there is no un-due variation of in the ``blue direction''). The equation of the ideal model is either:

or

or  or

or

. Note that, inside figure 2

(and also 1), we do NOT have exactly

. Note that, inside figure 2

(and also 1), we do NOT have exactly

(the green point are not totally on the dashed line

(the green point are not totally on the dashed line

). Thus, we theoretically have enough information

in the ``blue direction'' to construct a model. However exploiting this information

to predict is not a good idea and leads to unstable models: a small perturbation

of the data ( or ) leads to a completely different model: Inside figure 2,

we have represented in red two models based on small perturbations of and . Usually, unstable models have poor accuracy. The main question now

is: How to stabilize a model? Here are two classical solutions:

). Thus, we theoretically have enough information

in the ``blue direction'' to construct a model. However exploiting this information

to predict is not a good idea and leads to unstable models: a small perturbation

of the data ( or ) leads to a completely different model: Inside figure 2,

we have represented in red two models based on small perturbations of and . Usually, unstable models have poor accuracy. The main question now

is: How to stabilize a model? Here are two classical solutions:

- Inside figure 1, the 'information' that is

contained in is duplicated in . We can simply drop one of the two variables. We obtain the models

or . The main difficulty here is to select carefully the columns

that must be dropped. The solution is the ``LARS/Lasso Algorithm'' described

later in this paper.

- The other choice is to keep inside the model

all the variables (

all the variables (

and

and

). However, in this case, we must be sure that:

). However, in this case, we must be sure that:

-

and

and  are small values (I remind you that and can become arbitrarily large).

are small values (I remind you that and can become arbitrarily large).

We must find an algorithm to compute that will ``equilibrate'' and ``reduce'' the 's:

is the solution of

|

(5) |

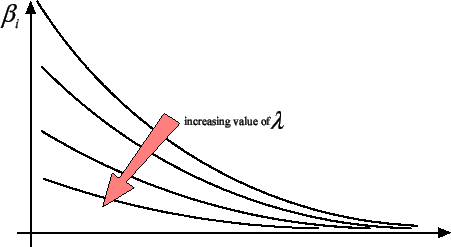

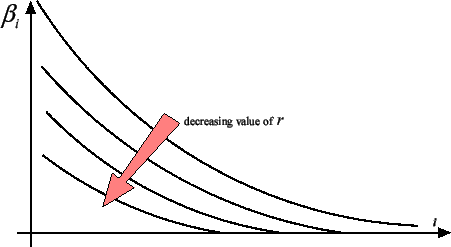

This technique is named ``Ridge regression''. When

increases, all the

are ``equilibrated'' and ``pushed'' to zero as illustrated

in figure

3.

Figure 3: The 's sorted from greatest to smallest for different value of

.

|

We will discuss later of a way to compute an optimal regularization parameter

. Inside figure

1, we obtain

the model

and we have thus

with

''small''.

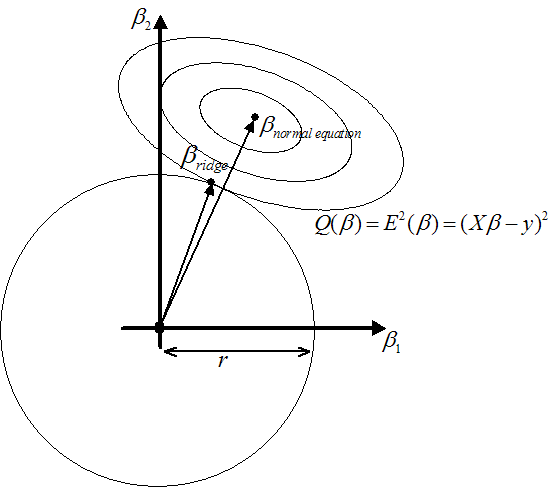

The ``Ridge regression'' technique is particularly simple and efficient. It has

a nice graphical explanation. The ``Ridge

regression'' technique is in fact searching for that minimizes

Squared Error

Squared Error under the constraint that

under the constraint that

. This definition is illustrated on the left

of figure 4.

We seek the solution of the minimization problem:

. This definition is illustrated on the left

of figure 4.

We seek the solution of the minimization problem:

subject to

(with  and

and  ) To solve this minimization problem, we first have to rewrite

the constraint:

) To solve this minimization problem, we first have to rewrite

the constraint:

. Now, we introduce

a Lagrange multiplier and the Lagrange function:

Using the Lagrange First order optimality criterion, we know that the solution

. Now, we introduce

a Lagrange multiplier and the Lagrange function:

Using the Lagrange First order optimality criterion, we know that the solution

to this optimization problem is given by:

to this optimization problem is given by:

|

(6) |

which is equation 5.

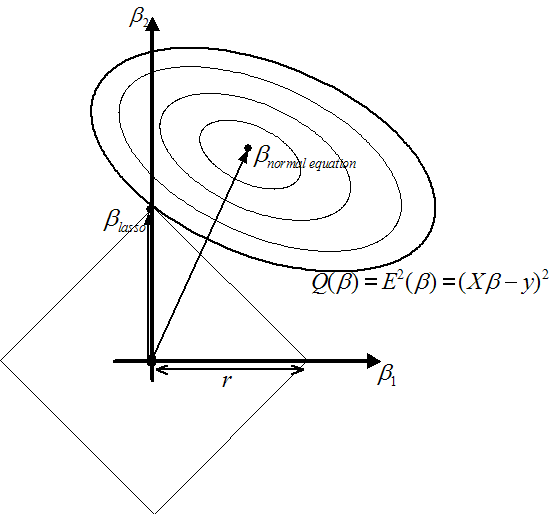

Figure 4: On the left: Illustration of Ridge Regression.

On the right: Illustration of Lasso

|

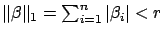

The constraint

prevents the 's from becoming arbitrarily large. As illustrated in figure

3, the ridge regression algorithm ``pushes'' all the

's towards zero but none of the actually gets a null value. It's interesting to have  because, in this case, we can completely remove from the

model the column . A model that is using less variables has many advantages: it is

easier to interpret for a human and it's also more stable. What happens if we

replace the constraint

with the constraint

because, in this case, we can completely remove from the

model the column . A model that is using less variables has many advantages: it is

easier to interpret for a human and it's also more stable. What happens if we

replace the constraint

with the constraint

? See the

right of illustration 4. You can see on the figure that

? See the

right of illustration 4. You can see on the figure that

with

with

. You can see on figure 5 that,

as you decrease

. You can see on figure 5 that,

as you decrease  , more and more

, more and more  are going to zero.

are going to zero.

Figure 5: The 's sorted from greatest to smallest for different values of

|

The Lasso regression is defined by: is the solution of the minimization problem:

subject to subject to  |

(7) |

As you can see, computing different 's (with a different number of null 's) involves solving several times equation 7

for different values of . Equation 7 is a QP (Quadratic Programming)

problem and is not trivial to solve at all. The Lasso algorithm, as it is described

here, is thus very demanding on computer resources and is nearly of no practical

interest. Hopefully, there exist another, more indirect, way to compute at a very

little cost all the solutions of the Lasso Algorithm for all the values of . A modification of the LARS algorithm computes all the Lasso solution

in approximatively the time needed to compute and solve the simple ``normal equations''

(equation 4) (the algorithmic complexity of

the two procedures is the same). LARS stands for ``Least Angle Regression laSso''.

We will not describe here the LARS algorithm but we will give an overview of some

of its nicest properties.

The LARS algorithm is a refinement of the FOS (Fast Orthogonal Search) algorithm.

We will start by describing the FOS algorithm. The FOS (and the LARS algorithm)

is a forward stepwise algorithm. i.e. FOS is an iterative algorithm that, at each

iteration, includes inside its model a new variable. The set of variables inside

the model at iteration  is the ``active set''

is the ``active set''

. The set of variables outside the model is the ``inactive set''

. The set of variables outside the model is the ``inactive set''

.

.

is a subset of column of containing only the active variables at iteration .

is a subset of column of containing only the active variables at iteration .

is a subset of column of containing only the inactive variables at iteration .

is a subset of column of containing only the inactive variables at iteration .

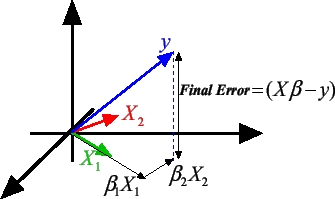

Let's first illustrate the equation 2: . Equation 2 can be rewritten:

|

(8) |

If

, then

is a column of X. can also be seen as a vector in a

is a column of X. can also be seen as a vector in a  dimensional space and

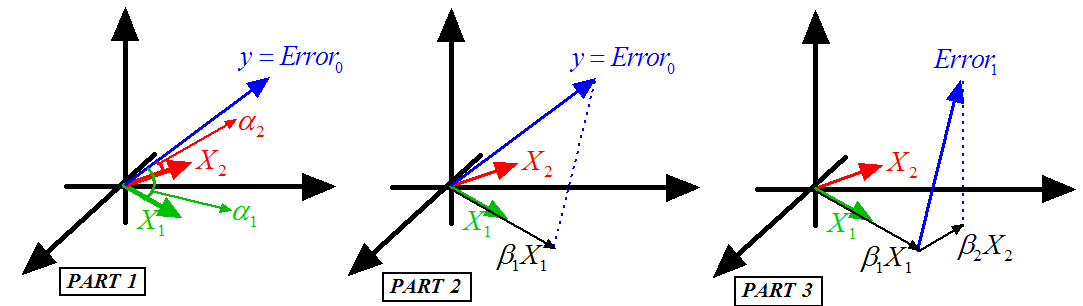

is the best linear combination of the vectors to reach the target . The ``vector view'' of equation 8 is illustrated

in figure 6 where

dimensional space and

is the best linear combination of the vectors to reach the target . The ``vector view'' of equation 8 is illustrated

in figure 6 where

Figure 6: Graphical interpretation of

|

The FOS algorithm does the following:

- Let's define the residual prediction error at step as

. We have

. We have  . Normalize the variables and the target to have

. Normalize the variables and the target to have

and

and  . Set

. Set  , the iteration counter.

, the iteration counter.

Figure 7: Illustration of the FOS algorithm

|

- This step is illustrated in figure 7, Part 1.

We will add inside

the variable that is ``the most in the direction of ''. i.e. the ``angle''

between

between  and is smaller than all the other angles

and is smaller than all the other angles  (

( ) between the 's and . Using the well-know relation:

) between the 's and . Using the well-know relation:

|

(9) |

Since the variables have been normalized, we obtain:

where where  |

(10) |

Note that  is simply the correlation between variable and the Residual Error .

is simply the correlation between variable and the Residual Error .

Thus the algorithm is: ``compute

. Find such that

. Find such that

|

(11) |

Add the variable to the active set

. Remove variable from the inactive set

''.

- This step is illustrated in figure 7, Part 2.

We now compute

, the length of the ``step'' in the direction (inside the example j=1). Let's project (orthogonally)

inside the space that is ``spanned'' by the active variables. The

projection of is named

, the length of the ``step'' in the direction (inside the example j=1). Let's project (orthogonally)

inside the space that is ``spanned'' by the active variables. The

projection of is named  . We obtain

. We obtain

since is normalized. If the projection operator fails ( is

since is normalized. If the projection operator fails ( is

inside the space spanned by the active set  of variables), remove from the active set

and go to step 2.

of variables), remove from the active set

and go to step 2.

- Deflation: update of the Residual Error:

.

.

- If

is empty then stop, otherwise increment and go to step 2.

Let's define  , the number of active variable at the end of the algorithm. If

you decide to stop prematurely (for example, when

, the number of active variable at the end of the algorithm. If

you decide to stop prematurely (for example, when

), you will have

), you will have  . The FOS algorithm has several advantages:

. The FOS algorithm has several advantages:

- It's ultra fast! Furthermore, the computation time is mainly proportional

to . If , then you will go a lot faster than when using the standard

normal equations.

- The algorithm will ``avoid'' naturally the correlated columns. I remind

you that a model that is using two strongly correlated columns is likely to

be unstable. If column and are strongly correlated, they are both ``pointing'' to the same direction

(the angle between them is small: see equation 9

and figure 6) . If you include inside the active

set the column , you will obtain, after the deflation, a new error

that will prevent you to choose at a later iteration. One interpretation is the following: ``All

the information contained inside the direction has been used. We are now searching for other directions to reach

''. It is possible that, at the very end of the procedure, the algorithm

still tries to use column . In this case, the projection operator used at step 3 will fail

and the variable will be definitively dropped. Models produced with the FOS algorithm

will thus be usually very stable.

that will prevent you to choose at a later iteration. One interpretation is the following: ``All

the information contained inside the direction has been used. We are now searching for other directions to reach

''. It is possible that, at the very end of the procedure, the algorithm

still tries to use column . In this case, the projection operator used at step 3 will fail

and the variable will be definitively dropped. Models produced with the FOS algorithm

will thus be usually very stable.

- The selection of the column that enters the active set is based on the ``residual

error'' at step (with

). This selection is thus exploiting the information contained

inside the target . The ``target information'' is not used by other algorithms that

are based on SVD of or QR factorization of . The FOS algorithm will thus performs a better variable selection

than SVD- or QR-based algorithm. Many other algorithms do not use any deflation.

Deflation is important because it allows us to search for variables that explains

the part of the target that is still un-explained (the residual error ). A good variable selection is useful when .

). This selection is thus exploiting the information contained

inside the target . The ``target information'' is not used by other algorithms that

are based on SVD of or QR factorization of . The FOS algorithm will thus performs a better variable selection

than SVD- or QR-based algorithm. Many other algorithms do not use any deflation.

Deflation is important because it allows us to search for variables that explains

the part of the target that is still un-explained (the residual error ). A good variable selection is useful when .

- The memory consumption is very small. To be able to use the FOS algorithm,

you only need to be able to store in memory the target , one line of , and a dense triangular matrix of dimension Other algorithms based on QR factorization of requires to have the full matrix inside memory because the memory space used to store is used during the QR factorization to store temporary, intermediate

results needed for the factorization. Algorithms based on SVD of are even more memory hungry. This is a major drawback for most advanced

applications, especially in Econometrics where we often have

. There exists some ``out of core'' QR and SVD factorizations that

are able to work even when does not fit into memory. However ``out of core'' algorithms are

currently extremely slow and unstable.

. There exists some ``out of core'' QR and SVD factorizations that

are able to work even when does not fit into memory. However ``out of core'' algorithms are

currently extremely slow and unstable.

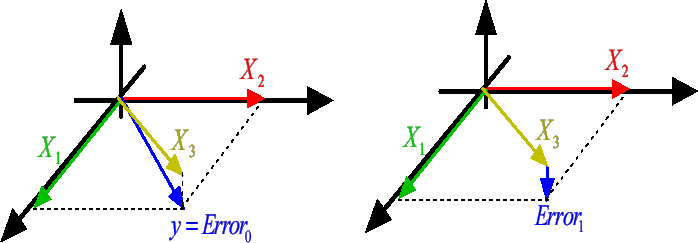

There is however one major drawback to the FOS algorithm. It is illustrated in

figure 8 where we have:

Figure: FOS algorithm fails and gives

|

At the first iteration, the FOS algorithm selects  because

because

is greater than

is greater than

(and

(and  . Thereafter, the FOS algorithm computes the new Residual Error

. Thereafter, the FOS algorithm computes the new Residual Error

and get stuck. Indeed, if we add to the active

set either or , the L2-norm of the Residual Error do not decrease:

and get stuck. Indeed, if we add to the active

set either or , the L2-norm of the Residual Error do not decrease:

. There is no way to add a new variable

to decrease the Residual Error and thus the algorithm stops. There are mainly

two conceptual reasons why the FOS algorithm fails:

. There is no way to add a new variable

to decrease the Residual Error and thus the algorithm stops. There are mainly

two conceptual reasons why the FOS algorithm fails:

- The FOS algorithm is a forward stepwise algorithm and, as almost all forward

stepwise algorithms, it is not able to detect multivariate concepts. In the

example illustrated in figure 8, the target is defined

precisely to be =+. You are able to predict the target accurately if your model is

. The FOS algorithm gives the wrong model

. In this example, the target is a multivariate concept hidden inside two variables: and . A forward stepwise algorithm that is able to detect a multivariate

concept is very difficult to develop. Inside FOS, the selection of the variable

that enters the active set is only based on the univariate relation

of with the target . On the contrary, Backward stepwise algorithms have no problem to

detect multi-variable concepts and should thus be preferred to a Simple,Classical

Forward Stepwise Algorithm. However, usually, Backward stepwise algorithms

are very time consuming because they need first to compute a full model and

thereafter to select carefully which variables they will drop.

. The FOS algorithm gives the wrong model

. In this example, the target is a multivariate concept hidden inside two variables: and . A forward stepwise algorithm that is able to detect a multivariate

concept is very difficult to develop. Inside FOS, the selection of the variable

that enters the active set is only based on the univariate relation

of with the target . On the contrary, Backward stepwise algorithms have no problem to

detect multi-variable concepts and should thus be preferred to a Simple,Classical

Forward Stepwise Algorithm. However, usually, Backward stepwise algorithms

are very time consuming because they need first to compute a full model and

thereafter to select carefully which variables they will drop.

The LARS algorithm with Lasso modification is a forward stepwise algorithm

that produces all the solutions of the Lasso algorithm in a computing time

proportional to ( is the number of active variable at the end of the algorithm).

The Lasso algorithm is part of the family of the backward stepwise algorithm

(It starts with a full model and remove some variables when decreases). Thus, the Lasso algorithm is able to discover multi-variable

concepts. And thus, the LARS algorithm with Lasso modification is also able

to discover multi-variable concepts (since LARS with Lasso gives the same

models than the Lasso algorithm). From my knowledge, the LARS algorithm with

Lasso modification is the only forward stepwise algorithm able to discover

multi-variable concepts. Since, it's a forward stepwise algorithm, it's also

very fast.

On the other side, conjunctive concepts are easy to detect. Let's assume that

you have the following:

If you create a column

(

(

), you obtain:

), you obtain:

and

i.e. You can represent conjunctive concepts with the product of variables.

You will thus obtain second order models. Computing second order models usually

involves extending the original matrix with columns that are the product of some of the columns of

the original . This is usually a very memory expansive operation. Indeed if is the number of column of , then the extended

matrix has

matrix has

columns. The LARS library has been built to allow

you to easily create ``on the fly'' a regressor (= one line of

). i.e. you only need to be able to store in memory one

line of

, not the whole

matrix. This allows you to compute at a low memory consumption

second, third, fourth,... order models.

columns. The LARS library has been built to allow

you to easily create ``on the fly'' a regressor (= one line of

). i.e. you only need to be able to store in memory one

line of

, not the whole

matrix. This allows you to compute at a low memory consumption

second, third, fourth,... order models.

- The FOS algorithm is ``too greedy'': when the FOS algorithm finds a good

direction, it is exploiting this direction ``to the maximum'' (the length

of the steps is

). Thereafter there is no ``room left'' for further

improvements, adding other variables. The FOS has been ``trapped'' in a so-called

``local optimum''. The LARS algorithm is not so greedy. Its steps lengthes

are shorter (see step 3. of the FOS algorithm about ``steps''). This means

that the different models that are computed at each steps of the LARS algorithm

are not 100% efficient. With the same set of active variables, one can compute

a better model. The LARS library downloadable on this page allows you to obtain

both models:

). Thereafter there is no ``room left'' for further

improvements, adding other variables. The FOS has been ``trapped'' in a so-called

``local optimum''. The LARS algorithm is not so greedy. Its steps lengthes

are shorter (see step 3. of the FOS algorithm about ``steps''). This means

that the different models that are computed at each steps of the LARS algorithm

are not 100% efficient. With the same set of active variables, one can compute

a better model. The LARS library downloadable on this page allows you to obtain

both models:

- the most efficient one.

- the one used inside the LARS algorithm to search for the next variables

to add inside the active set.

To resume, the LARS algorithm has all the advantages of the FOS algorithm:

- ultra fast.

- correlated columns are avoided to obtain stable models.

- Selection of the active variables based on the target (Deflation).

- small memory consumption.

Furthermore, the LARS algorithm with Lasso modification is able to discover multivariate

concepts easily. For example, the LARS algorithm with LASSO modification finds

for the example illustrated in figure 8 .

There exists one last question to answer when using the LARS algorithm: When to

stop? How to choose ? The question is not simple. Several strategies are available inside

the LARS library downloadable on this page:

My advice is :

- to choose a very stringent termination test (like the first one with

) to be sure to have all the informative variables.

) to be sure to have all the informative variables.  has a nice and easy interpretation: it's the percentage of

has a nice and easy interpretation: it's the percentage of

the variance inside that will not be explained.

- to perform a backward stepwise, using as initial model, the model given

by the LARS algorithm. The LARS library has been designed so that such task

is very easy to code.

My experience is that stopping criterions based on MDL (maximum description

length), Akkaike index or  statistics are not reliable.

statistics are not reliable.

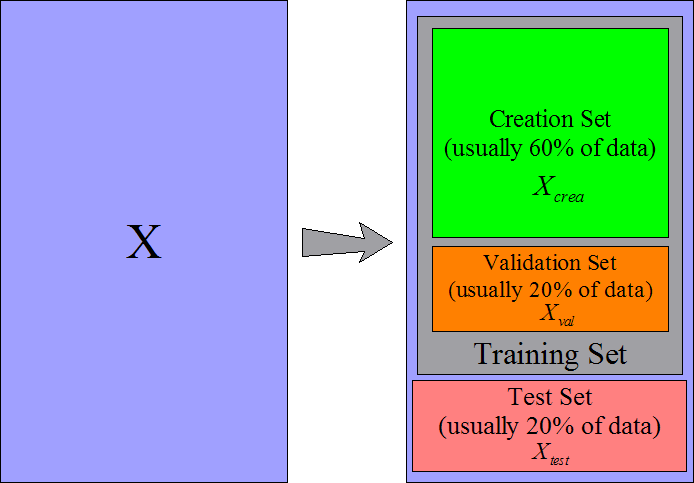

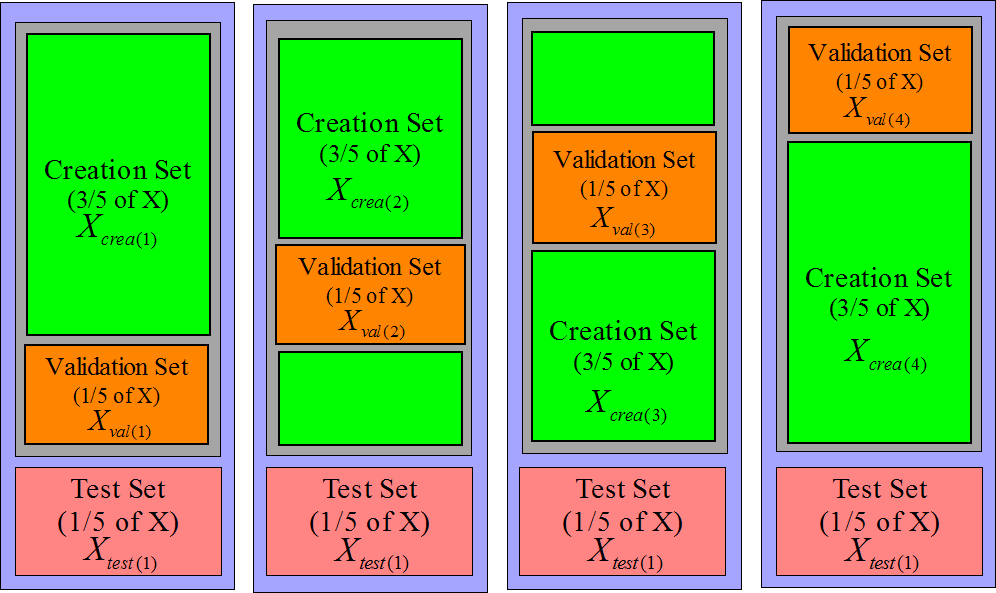

To be able to answer the simple question ``How good is my model?'' you need a

good methodology. Let's assume that we have a set of data and . You will cut this data in three parts: a creation set  , a validation set

, a validation set  and a test set

and a test set  . The procedure is illustrated in figure 9.

. The procedure is illustrated in figure 9.

Figure 9: Data are cut into three parts

|

The creation set will be used to build a first model. You can build the model

using the normal equation (

) or using the LARS algorithm. Thereafter

the model needs to be stabilized (stabilization is less important if you

have built the model with the LARS algorithm but can still improve a little your

model). There are mainly two simple ways to stabilize a model: Remove un-informative

variables (this is called ''backward stepwise'') and Ridge Regression.

) or using the LARS algorithm. Thereafter

the model needs to be stabilized (stabilization is less important if you

have built the model with the LARS algorithm but can still improve a little your

model). There are mainly two simple ways to stabilize a model: Remove un-informative

variables (this is called ''backward stepwise'') and Ridge Regression.

To remind you, the Ridge Regression is based on equation 5:

|

(17) |

where is the regularization parameter that needs to be adjusted,

is the model (depending on the value of ) and is the creation set. If is high, the model will be strongly stabilized. The optimal

value of the parameter is

is the model (depending on the value of ) and is the creation set. If is high, the model will be strongly stabilized. The optimal

value of the parameter is  . is the solution to the optimization problem:

where

is computed from equation 17.

We are searching for the value of that gives the best model when applied on the validation set.

We are improving the ``generalization ability'' of our model. Since we never used

any data from the validation set to build our model, the performance of the model

is entirely due to its ``generalization ability''.

. is the solution to the optimization problem:

where

is computed from equation 17.

We are searching for the value of that gives the best model when applied on the validation set.

We are improving the ``generalization ability'' of our model. Since we never used

any data from the validation set to build our model, the performance of the model

is entirely due to its ``generalization ability''.

To stabilize your model, you can also completely remove some variables using a

``backward stepwise'' algorithm. Here is a simple ``backward stepwise'' algorithm:

- Let's define

, the creation set without the column . Let's define

, the creation set without the column . Let's define

where is the solution to the standard normal equation:

where is the solution to the standard normal equation:

.

.  is the performance on the validation set of a model using all the columns of the creation set . Set

is the performance on the validation set of a model using all the columns of the creation set . Set  .

.

- We will try to remove the variable . Compute

, the solution to

, the solution to

. Compute

. Compute

: the performance of

the model

on the validation set when the model is built without taking into account the column of the creation set . If

: the performance of

the model

on the validation set when the model is built without taking into account the column of the creation set . If

, then the column did not contain any information and can be dropped: Set

, then the column did not contain any information and can be dropped: Set

.

.

- Choose another and go back to step 2.

Let's define

, the optimal set of column after the backward stepwise.

Once we have found an optimal ridge parameter and/or the optimal set

of informative columns (backward stepwise), we can

compute the final model using:

|

(18) |

where  contains only the columns in

.

contains only the columns in

.

WARNING: If you try to use both regularization techniques at the same time, they

will ``enter in competition''. You should then be very careful.

To get an idea of the quality of your final model , you can apply it on the test set:

Squared Error on test set=

The methodology just described here is a correct approach to a modelization problem.

However, this approach does not use a very large validation and test set. Since

the validation set is small, the parameter and the set

of active columns will be very approximative. Since

the test set is small, the estimation of the quality of the model is also very

approximative. To overcome these difficulties, we can use a n-fold-cross-validation

technique. If we want a more accurate estimation of the quality of the model,

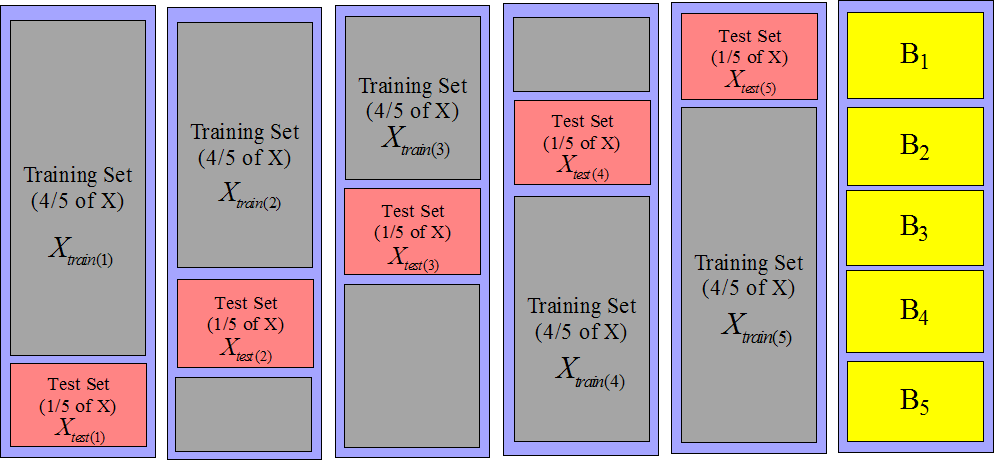

we can build 5 test sets instead of one: see figure 10.

It's named a 5-fold-cross-validation. It also means that we have 5 training sets

and thus 5 different models. The main point here is that none of these 5 models

have seen the data that are inside their corresponding test set.

Figure 10: 5 test sets (and 5 training sets))

|

An estimation of the overall quality of our modelization is:

| |

|

|

| |

where

is the solution to is the solution to  |

(19) |

where

and

and

are defined on figure 10.

are defined on figure 10.

When we perform a n-fold-cross-validation, we must compute different models

using equation 19.

The only time-consuming part inside equation 19 is

the computation of

using equation 19.

The only time-consuming part inside equation 19 is

the computation of

. Here is a small ``trick'' to be able to compute

. Here is a small ``trick'' to be able to compute

in a very efficient way:

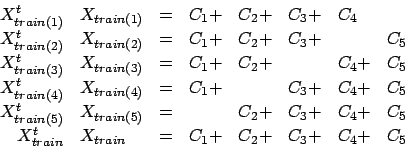

If we define

in a very efficient way:

If we define  as in figure 10, we can compute

as in figure 10, we can compute

. Then, we have:

. Then, we have:

|

(20) |

Thanks to equations 20, we can compute

very easily: only a few matrix

additions are needed. The same property of addition exist for the right hand side

of equation 19:

. Since solving equation 19 is instantaneous

on modern CPU's (only the computation of

. Since solving equation 19 is instantaneous

on modern CPU's (only the computation of

is time-consuming), we can easily obtain the

is time-consuming), we can easily obtain the

different models

and the n-fold-cross-validation is ``given nearly for free''.

different models

and the n-fold-cross-validation is ``given nearly for free''.

The same technique can be applied to increase the size of the validation set:

see figure 11.

Figure 11: 4 validation sets (and 4 creation sets))

|

When building a model, the first step is the normalization of all the variables

(the columns ). The normalization of a variable consist of two steps:

- We subtract from the column its mean

- We divide the column by its standard deviation

Thereafter the

are computed: see equation 20 and

figure 10. Based on the

are computed: see equation 20 and

figure 10. Based on the  's we can compute easily many different models

. Let's assume that we want a model that is completely ignoring

the block

's we can compute easily many different models

. Let's assume that we want a model that is completely ignoring

the block  : the block will be used as test set. Referring to figure 10,

the test set is

: the block will be used as test set. Referring to figure 10,

the test set is

and the training set is

and the training set is

. The columns in block

. The columns in block  have been normalized using and . The two parameters and are partially based on information contained inside the block

. We are breaking the rule that says:

have been normalized using and . The two parameters and are partially based on information contained inside the block

. We are breaking the rule that says:

| ``never use any information from the test set

to build a model'' |

(21) |

The columns in (part of the creation set) are normalized using information from

(the test set). This small ``infraction'' of the rules is usually

negligible and allows us to reduce considerably the computation time. However,

for some rare variables, the rule must be respected strictly. These variables

are named ``dynamic variables''. The LARS library does a strong distinction between

``dynamic variables'' and ``static variables''. The LARS library handles both

types of variables. However only the ''static variables'' are reviewed inside

this documentation.

The concept of ``dynamic variables'' is linked with the concept of ``variable

recoding''. The normalization of the variables is a (very basic) recoding. If

there is no recoding, there is no ``dynamic variables''. The ``normalization of

a variable'' is a recoding that never produces any ``dynamic variables'' (especially

if all the lines of have been correctly scrambled). ``Dynamic variables'' appears mostly

when using advanced recodings such as, for example, in the paper ``1-Dimensional

Splines as Building Blocks for Improving Accuracy of Risk Outcomes Models'' by

David S. Vogel and Morgan C. Wang. The LARS library is handling advanced recodings

through the use of ``dynamic variables''.

Inside the LARS library, the parameter of the Ridge Regression is computed using a n-fold-cross-validation

on the validation sets. Equations 20 are used to achieve

high efficiency. The

matrices are built incrementally each

time a new variable enters the active set

. The equations 19 are solved

using an advanced Cholesky factorization that is using an advanced pivoting strategy

and an advanced perturbation strategy to obtain a very high accuracy model even

when the matrices

matrices are built incrementally each

time a new variable enters the active set

. The equations 19 are solved

using an advanced Cholesky factorization that is using an advanced pivoting strategy

and an advanced perturbation strategy to obtain a very high accuracy model even

when the matrices

are close to singularity or badly conditioned.

are close to singularity or badly conditioned.

The LARS library has been written to use the less memory possible. For example,

all the matrices are symmetric, thus we only need to store half of these

matrices in memory. ``In place'' factorization of matrices have been used when

possible.

It can happen inside the LARS forward stepwise algorithm that several variables

should enter the active set

at the same iteration (there are several values of that are possible inside equation 11 ).

It can also happens that several variables should leave the active set

at the same iteration . Most algorithms do not treat correctly these special cases. The

LARS library is handling correctly these cases.

The usage is:

[betaBest,betas,errors,cHats]=matlabLARS(X,y,stoppingCriteriaType,stoppingCriteriaValue,lassoModif, verbosity);

matlabLARS is an iterative algorithm that compute different 's  such that

such that

is minimum (classical least-square). The X

matrix and the y vector do not need to be normalized.

is minimum (classical least-square). The X

matrix and the y vector do not need to be normalized.

At the first iteration only one is non-null. At each iteration , we will:

- set one more to a non-null value.

- compute Error

where Error

where Error

- compute cHat=

(see equation 13 about )

(see equation 13 about )

The different 's, computed at each iterations, are stored inside the matrix

'betas'. The best model among all the models according to the selected

stopping criteria is stored in 'betaBest'. In a similar way, at each

iteration, the squared error Error and the maximum correlation values cHat, are stored respectively

inside the matrices 'errors' and ' cHats'.

If the lasso modification is used (set lassoModif=1), then some could be reset to a null value at some rare iterations.

Let's define cHat(k) the value of cHat at iteration .

Let's define sqEr(k) the value of Error at iteration .

Let's define n(k) the number of non-null at iteration .

The variable 'stoppingCriteriaType' is a character that can be:

- 'R': if ((cHat(k-10)-cHat(k))< stoppingCriteriaValue cHat(0)),

then stop

- 'S': if ((sqEr(k-10)-sqEr(k))< stoppingCriteriaValue sqEr(0)),

then stop

- 'C': Cp test: Let's define

- Cp(k) = sqEr(k)-nCol+2*n(k)

- p =stoppingCriteriaValue

if (Cp(k)> max Cp(k-p), Cp(k-p+1),..., Cp(k-1)), then stop

- 'M': Let's define minCVError(k) as the 6-Fold-Cross-Validation-Error

of a model beta(k) that has been regularized using an optimized ridge

parameter

.

.

if (minCVError(k)>minCVError(k-1)), then stop

- 'E': if (stoppingCriteriaValue=-1) include all columns, otherwise:

if (number of non-null =stoppingCriteriaValue), then stop

The variable 'verbosity' is optional. It's a number between 0 and

2. (2=maximum verbosity).

As previously mentioned, if you select a specific set of active variable, you

can compute at least two different models :

- the most efficient one (stored inside betaBest)

- the one used inside the LARS algorithm to search for the next variables

to add inside the active set (stored inside betas).

betaBest is the constant term of the model. All the models (in betas

and betaBest) are computed to be applied on un-normalized data.

is the constant term of the model. All the models (in betas

and betaBest) are computed to be applied on un-normalized data.

The Matlab interface to the LARS library is very poor compared to the C++ interface.

The source code of the matlab interface (in C++) is inside the zip-file downloadable

at the top of this webpage. If you want to customize the Matlab version of the

LARS library, it's very easy to edit/modify this small C++ code. The C++ interface

is documented below.

Inside the zip-file downloadable inside this webpage, you will find the source

code of a small C++ executable that solves the `diabetes' example. The `diabetes'

data are stored inside an external .csv file. The last column of the

.csv file is the target. A very fast .csv-file-reader is provided.

It's very easy to edit/modify the small C++ code to customize it to your needs.

The C++ interface is documented below.

The LARS library is available as a .dll file. To use this .dll

file in your own project you must:

- In the ``debug'' version of you program, add inside the ''Linker/Input/Additional

Dependencies'' tab: ``larsDLLDebug.lib''

- Inside the directory containing the executable of the ''debug'' version

of you program, add the file ''larsDLLDebug.dll''

- In the ``release'' version of you program, add inside the ''Linker/Input/Additional

Dependencies'' tab: ``larsDLL.lib''

- Inside the directory containing the executable of the ''release'' version

of you program, add the file ``larsDLL.dll''

- Add inside your project the files ``lars.h'' and ''miniSSEL1BLAS.h''

In order to work, the LARS library must access the matrix and the vector. The normalization of and is done automatically inside the LARS library, if needed. You can

provide the data ( and ) in two different ways:

- Line by Line: You must create a child of the LARS

class. Inside the child class, you must re-define some of the following functions:

- larsFLOAT *getLineX(int i, larsFLOAT *b);

This function return the line of . The required line can be stored inside the b array or inside

an other array. A pointer to the array containing the line must be returned.

- larsFLOAT getLineY(int i);

This function return the component of :  . Alternatively, you can use the third parameter of the getModel

function to specify a target.

. Alternatively, you can use the third parameter of the getModel

function to specify a target.

- void setSelectedColumns(int n,int *s);

The re-definition of this function is optional. The default implementation

is:

void LARS::setSelectedColumns(int n,int *s) { selectedC=s; nSelected=n; }

The setSelectedColumns function announces that subsequent calls

to the function getLineXRequired will return only a part of the

column of . The indexes of the columns that should be returned are given inside

the array s of length n.

- larsFLOAT *getLineXRequired(int i, larsFLOAT *b);

The re-definition of this function is optional. However, it's strongly

recommended that you re-define this function for performance reasons.

The default implementation is:

larsFLOAT *LARS::getLineXRequired(int i, larsFLOAT *b)

{

int j,ns=nSelected, *s=selectedC;

larsFLOAT *f=getLineX(i,b);

for (j=0; j<ns; j++) b[j]=f[s[j]];

return b;

}

This function returns only the columns of line i that have been

selected using the function setSelectedColumns.

- Column by Column: You must create a child of the LARS

class. Inside the child class, you must re-define the following functions:

- larsFLOAT *getColX(int i, larsFLOAT *b);

This function return the column of . The required column can be stored inside the b array or

inside an other array. A pointer to the array containing the line must

be returned.

- larsFLOAT *getColY(larsFLOAT *b);

This function return the target . The target can be stored inside the b array or inside an other array.

A pointer to the array containing must be returned. Alternatively, you can use the third parameter

of the getModel function to specify a target.

Let's now assume that you have created a child of the base LARS class

named LARSChild. You can now configure the different parameters of the

LARS algorithm. Typically, you define these parameters inside the constructor

of LARSChild. The parameters are:

- nCol: the number of column of .

- nRow: the number of rows of .

- orientation: if orientation='L', then we access the matrix line by line. Otherwise, we access the matrix column by column.

- lasso: if lasso=1, then the lasso modification of the

LARS algorithm is used.

- fullModelInTwoSteps: if fullModelInTwoSteps=1, then no

forward stepwise is performed: we are directly building a model using all

the column of . When the number of column nCol is small this is faster

than the full LARS algorithm.

- ridge: if ridge=1, then an optimization of the parameter of the ridge regression is performed at the end

of the build of the model (this requires

).

).

- memoryAligned: all the linear algebra routines are SSE2 optimized.

This means that the functions getCol* and getLine* should

return a pointer to an array that is 16-byte-memory-aligned. Such an array

ca be obtained using the mallocAligned function of the miniSSEL1BLAS

library. If you are not able to provide aligned-pointers, you can set

memoryAligned=0, but the computing time will be more or less doubled.

- nMaxVarInModel: maximum number of variables inside the model when

performing a forward stepwise (this is a stopping criteria).

- nFold: the number of block (as defined in figure 10) for the n-fold-cross-validation.

- folderBounds: an array of size

of integer that contains the line-index of the first line of

each (as defined in figure 10). We should

also have folderBounds[nFold]=nRow. If you don't initialize this

parameter, then folderBounds will be initialized for you automatically

so that all the blocks have the same size.

of integer that contains the line-index of the first line of

each (as defined in figure 10). We should

also have folderBounds[nFold]=nRow. If you don't initialize this

parameter, then folderBounds will be initialized for you automatically

so that all the blocks have the same size.

- stoppingCriteria: define which kind of stopping criteria will be

used inside the forward stepwise:

- stoppingCriteria='R': stop based on the maximum correlation

of the inactive columns with the residual error. see equation 13

with

of the inactive columns with the residual error. see equation 13

with  stopSEP.

stopSEP.

- stoppingCriteria='S': stop based on the L2-norm of the residual

error

: see equation 14 with

: see equation 14 with  stopSEP.

stopSEP.

- stoppingCriteria='C': stop based on the

criterion: see equation 15 with

criterion: see equation 15 with  stopSEP.

stopSEP.

- stoppingCriteria='M': stop based on the n-Fold-cross-validation-Error

of the model: see equation 16.

Further configuration of the stopping criteria is available through the re-definition

inside the class LARSChild of these two functions:

- void initStoppingCriteria(larsFLOAT squaredError, larsFLOAT cHat);

This function is used to initialize internal variables for the stopping criteria.

- char isStoppingCriteriaTrue(larsFLOAT squaredError, larsFLOAT cHat,

larsFLOAT *vBetaC, LARSSetSimple *sBest);

If this function returns '1', the LARS forward stepwise algorithm stops. If

this function returns '0', the LARS algorithm is continuing. This function

update the object sBest. Typically, when a good selection of variable

is found we do: sBest->copyFrom(sA);. The final model contains

only the variables inside sBest.

This is all for the configuration of the LARS library! Now we are describing the

outputs. Before using any of the outputs, you must initialize and compute many

intermediate results. This is done through the function getModel that

is usually called on the last line of the constructor of the LARSChild

class. The prototype of the getModel function is:

larsFLOAT *getModel(larsFLOAT **vBetaf=NULL, LARSSetSimple *sForce=NULL, LARSFloat

*target=NULL, LARSError *errorCode=NULL);

You usually call it this way:

larsFLOAT *model=NULL;

LARSSETSimple sForce(1); sForce.add(3);

getModel(&model,&sForce);

This means that the LARS library will construct a model that will be returned inside the array pointed by model

(you must free this array yourself). The model will be ``forced'' to use the column

3. The LARSSETSimple class is a class that contains a set of indexes

of columns of .

Here is a detailed description of the parameters of getmodel:

- First parameter [output]: This parameter describes an array that

will be used to store the model. In the example above model was set

to NULL, so the getModel function allocates itself the memory needed.

You can allocate yourself the memory used to store the model: for example:

larsFLOAT *model=(larsFLOAT*)mallocAligned((nCol+1)*sizeof(larsFLOAT));

getModel(&model);

- Second parameter [input]: Describes the set of variables that will

be added inside the model. If you use the forward stepwise algorithm and if

you stop prematurely, this set of variable will be added to the active variables.

Of course, adding a variable that is already active will have no effect.

- Third parameter [input]: Describes the target. This should be an

array allocated with:

larsFLOAT *target=(larsFLOAT*)mallocAligned(nRow*sizeof(larsFLOAT)+32);

The LARS library will free this array for you at the right time. If

you use this parameter and if (stoppingCriteria 'M'), then the LARS library will not use the getColY

or the getLineY functions (you don't have to define them).

'M'), then the LARS library will not use the getColY

or the getLineY functions (you don't have to define them).

- Fourth parameter [output]: an error code that can be interpreted

using the getErrorMessage function.

Here is a detailed description of the (some of the) outputs:

- sA: you don't have direct access to the content of sA.

Usually, you do the following:

getModel();

LARSSETSimple sInModel(sA);

The object sInModel contains the set of indexes of all the

columns that are used inside the final model.

- invStdDev: this is an array that contains the inverse of the standard

deviation of all the columns of . If you have normalized yourself the column of (so that

), this array is NULL.

- invStdDevY: the inverse of the standard deviation of .

- mean: this is an array that contains the mean of all the column

of . If you have normalized yourself the column of (so that mean of

), this array is NULL.

), this array is NULL.

- meanY: the mean of .

- lambda: the optimal ridge parameter .

- target: the residual error

at the end of the LARS algorithm (NOT normalized).

at the end of the LARS algorithm (NOT normalized).

Here is a small sketch of a backward stepwise algorithm:

- Build a model using the getmodel function. Stop prematurely. The

index of the active variables are stored inside sA.

- Try to remove variable :

- Get a copy sCopy of all the variable inside the model: sCopy.copyrom(sA);

- Remove variable from sCopy: sCopy.remove(i);. Let's define na,

the number of variable inside sCopy: int na=sCopy.n;.

- This computes a model using only the columns inside sCopy:

larsFLOAT *vBeta=(larsFLOAT*)malloc((nCol+1)*sizeof(larsFLOAT));

buildModel(vBeta, lambda, -1, &sCopy);

A model in ``compressed/short form'' is stored inside the array vBeta.

vBeta is currently an array of size na. vBeta[j]

is the weight of the model given to the column of index sCopy.s[j]

The short form is a very efficient way of storing the model when combined

with functions such as getLineXRequired. To convert the model

to the ``normal/long form'', use: shortToLongModel(vBeta);

Note that the size of the ``long form'' of the model is nCol+1

because we need also to store the offset(constant term) of the model.

Inside this example the model is built using all the blocks (see figure 10 for a definition of

the 's). If we want to build a model using all the blocks except the block  , we will do: buildModel(vBeta, lambda, 4, &sCopy);

This allows us to perform easily a n-fold-cross-validation-error test.

, we will do: buildModel(vBeta, lambda, 4, &sCopy);

This allows us to perform easily a n-fold-cross-validation-error test.

- Test the model to see if we can remove column without having a loss of efficiency. This test may involves a n-fold-cross-validation

technique. If this is the case, we can drop definitively the column : we do: keepVars(sCopy); (sA will be updated).

- choose another column inside sA and go back to the first point of step 2.

As illustrated above, thanks the buildModel function, we can obtain easily

up to nFold different models based on the same set sA of variables.

Using the function buildAverageModel, we can compute one last model

that is the average of these nFold

different models. This last model

is a little bit less performant than the other models

but it is a lot more stable.

that is the average of these nFold

different models. This last model

is a little bit less performant than the other models

but it is a lot more stable.

To summarize, there is at least nFold+3 different models based on the

same set sA of variables:

- The model that is produced by the forward stepwise LARS algorithm when searching

for informative variables inside the stepwise iterations. This model is suboptimal

(see remark about ``greedy'' algorithms to know why). You can access this

model through the isStoppingCriteriaTrue function.

- The model given by the function buildModel(

): this model is using all the blocks inside the creation set.

): this model is using all the blocks inside the creation set.

- The models given by the function buildModel(

i): these models are using all the

the creation set minus the block . There are nFold models of this type (

i): these models are using all the

the creation set minus the block . There are nFold models of this type (

nFold-1).

nFold-1).

- The model given by the function buildAverageModel that is an average

of the nFold models computed using a n-fold-cross-validation technique.

If you give  as second parameter of the buildModel function,

no model stabilization through the ridge technique is performed. If you give

as second parameter of the buildModel function,

no model stabilization through the ridge technique is performed. If you give

lambda as second parameter of buildModel,

the optimal value stored in lambda is used to stabilize the

model. Each time you remove a variable from the model, you should recompute

lambda: this is done through the function minimalCrossValError.

lambda as second parameter of buildModel,

the optimal value stored in lambda is used to stabilize the

model. Each time you remove a variable from the model, you should recompute

lambda: this is done through the function minimalCrossValError.

Here are some more useful functions:

- larsFLOAT normalizedLinearCorrelation(int i, int j, int cv=-1);

This will return  : the linear correlation between variable and :

: the linear correlation between variable and :

. The result is normalized so that

. The result is normalized so that

. If cv=4, then the block is ignored while computing .

. If cv=4, then the block is ignored while computing .

- larsFLOAT linearCorrelationWithTarget(int i, int cv=-1);

This will return  : the linear correlation between variable and the target :

: the linear correlation between variable and the target :

. The result is normalized so that

. The result is normalized so that

. If cv=4, then the block is ignored while computing .

. If cv=4, then the block is ignored while computing .

- static larsFLOAT apply(int n, larsFLOAT *line, larsFLOAT *model);

This computes

![$ \displaystyle \sum_{i=0}^{i<n}

line[i]*model[i]+model[n]$](imgLARS/img295.png) (usually n=nCol).

(usually n=nCol).

You get two examples of use when you download the LARS Library:

- The source code of a matlab mex-file function based on the LARS library.

This allows you to use the LARS Library under Matlab. Due to limitation of

Matlab, we have to set the options orientation=`C' and memoryAlignment=0.

Thus, the library will be rather slow compared to a full C++ implementation.

The classical `diabetes' example is given (the same one than inside the main

paper on LARS). An evolution of the example illustrated in figure 8,

is also given. This example is interesting because the FOS algorithm fails

on it. The final model of the FOS algorithm contains only one variable: the

variable. On the contrary, the LARS algorithm is able to find the

right set of active variables: and .

- The source code of a small C++ executable that solves the `diabetes' example.

The `diabetes' data are stored inside an external .csv file. The

last column of the .csv file is the target. A very fast .csv-file-reader

is provided.

The functionalities of this library are still not completely documented. There

are many other functionalities linked to the correct usage of a ``rotating'' validation

set (''rotating'' means a n-fold-cross-validation validation set). Currently,

the documentation covers only the case of a ``rotating'' test set.

The documentation does not cover the ``dynamic variables'' (see equation 21

about ``dynamic variables'').

The library allows you to construct second order, third order,... models very

easily.

If memoryAlignment=1, all the matrix algebra are performed using an optimized

SSE2 library. If orientation=`L' and memoryAlignment=1, the

computation time is divided by two compared to memoryAlignment=0. In

this case, it's important to store the data ``line by line'' otherwise we lose

the ``locality'' of the computations. ``Locality'' means that all the data needed

to perform a large part of the computations are inside the (small) cache of the

processor. From a memory consumption standpoint, the ``line by line'' mode is

better. For all these reasons, the ``line by line'' mode is preferable to the

``column by column'' mode.

Inside the LARS algorithm, the Cholesky factorizations are performed incrementally

as new variables enter the model. The Cholesky factorizations are based on the

paper ``A revised Modified Cholesky Factorization Algorithm'' by Robert B. Schnabel

and Elisabeth Eskow. This advanced Cholesky Factorization allows us to obtain

high accuracy models even when close to rank deficiency.

The optimization of the ridge parameter is performed using a modified Brent algorithm to ensure global

convergence. The optimization algorithm has been extracted from an optimization

library named CONDOR.

Some papers about the Fast-Orthogonal-Search:

An easy, experimental and fun paper about model stabilization via Ridge: ``The

refmix dataSet'', Mark J.L. Orr.

A paper about Lasso: ``Regression shrinkage and

selection via the lasso'', Robert Tibshirani

A paper about LARS: ``Least Angle

Regression'', Bradley Efron, Trevor Hastie, Iain Johnstone and Robert Tibshirani

Cholesky factorization is based on the paper ``A

revised Modified Cholesky Factorization Algorithm'' by Robert B. Schnabel

and Elisabeth Eskow.

A very good advanced recoding: ``1-Dimensional

Splines as Building Blocks for Improving Accuracy of Risk Outcomes Models''

by David S. Vogel and Morgan C. Wang.

and

and  and

and